OK, let’s put that more politely. ” Cutting welfare spending is not only morally bankrupt, it’s economic vandalism”. Here’s why.

“Welfare benefits”. Those words are deliberately chosen to cast the recipients as “weak”, “scroungers”, etc. “Benefits” has come to suggest something idle feckless people have as a nice little extra earner to make life easy. “Welfare benefits” is now used to mean what used to be called “social security”, the idea that society as a whole looks after those in need of some help. Just like a large family gives help to a family member who has suffered a setback.

(Why do some people resent and make snide remarks about this idea? A curious and not very savoury quirk of psychology? The belief that people who are strong and work hard will never need financial help? Tell that to someone who develops a neurological condition, or is made redundant when a whole industry contracts.)

In the words (read here) of Emeritus Professor of Accountancy Richard Murphy: “If you ask the average politician about benefits, they will in some way or other imply that we are pouring money into a black hole and we’ve got to cut them, because that’s the only way in which the government can balance its books, and apparently the government balancing its books is vital for economic growth.” Read the full article here.

He goes on to say: “All of that is complete and utter nonsense. The actual reality is that making benefit payments in the UK is one of the best ways that we have available to us to stimulate growth in this country.” Read on to find out why that is.

After WW11, the wise and visionary government of that time established a system by which “society” (meaning, the UK State) would for the first time in UK history make provision to extensively protect the population from the hardship and poverty that might result from old age, ill-health, disability, and the episodes of unemployment that often arose from changes in the economic cycle. This was part of an updated comprehensive “National Insurance” scheme.

So, income to protect those people was administered by the Ministry for Social Security, which in 1968 became part of the Department of Health and Social Security. (I worked in a local office in the early 1970s).

The system then had two components, “supplementary pension” which was a top-up for pensioners to the state pension, assessed on their individual income and outgoings. The other being “supplementary benefit”, providing either a top-up or main income for those under pension age. The principle, more or less, amounted to a guaranteed minimum income, depending on a person’s circumstances.

“Ah, but the cheats” is often heard. Okay, let’s face it, there exists a small minority who cheat or abuse the system. Always has been, always will be. But that in no way justifies a hard line on the vast majority who actually, often desperately, need that money. Or cutting the overall level of social security payments, either by actual cuts, or by stealth by failing to update for inflation.

“The cost of welfare is unsustainable” is so often heard. Politicians of every major Party, cheered on by media pundits.

Not only is this a falsity based on the “household budget” fiction that has been drummed into us for decades- but it dishonestly suggests that the money paid for benefits somehow disappears down some black hole, and is lost to the economy- when the reverse is the case. (As so often, we’re being conned.)

Why is “unsustainable” utter bollocks? Here’s a neat summary by AI overview via google: “Spending by benefit recipients stimulates the economy by increasing consumer demand, which supports businesses and employment. This spending also generates tax revenue for the government through VAT, corporation tax, and income tax paid by the businesses and their employees. By ensuring recipients have money to spend, the benefits help to “fuel government revenue” and are not “lost,” contributing to economic stability and growth. (more details- see note 2)

It’s not difficult to understand, is it? People on benefits, eg Universal Credit, pay their bills like everyone else, and then spend what’s left. They buy what they need from the shops which sustains small and large retail businesses. Sometimes have to replace clothing/do household repairs. While out shopping, may pop into low-cost cafes, Save up for family occasions, etc. A lot of this spending incurs V.A.T, so they’re paying tax. The employees of the businesses they sustain pay income tax, and the businesses Corporation and other taxes- so, a hell of a lot (or all eventually) is drained out of the economic system to balance spending. But most importantly, after helping to drive those businesses into prosperity, which feeds on itself.

“Nonetheless, though, however it is looked at, the vast majority of the benefit payments in the UK go to people on lower incomes. And if there’s one thing that we know about people in the UK who are on lower incomes, it is that they have very few savings. Only 9% of UK wealth is owned by people in the bottom half of the income distribution. And as a consequence, what we know is that the vast majority of the money that they get month in, month out is spent by them and virtually straight away.”(Murphy.)

When the wealthy get more money, they might buy a few more luxury goods, but they stash away most of it. That money, in savings accounts or financial investments, doesn’t do any good to the rest of our economy, it just sits there. “But if we start injecting money instead into the economy with those who are amongst the poorest benefit recipients, what we can guarantee is that we get the maximum payback on that money because it will circulate many more times before the wealthy get their hands on it, put it aside, and break the cycle of growth, which it gives rise to.”(Murphy)

How great is this boost to the economy? Economists talk about the “multiplier effect”, which is the multiple by which the general economy is, pound for pound, stimulated by government investment in any given sector. Richard Murphy estimates thst for benefits, that multiplier is x3. (It is generally thought that the multiplier for the NHS is x4). That means that every £1 paid in social security generates (approx) £3 worth of economic activity in the country’s economy.

And while doing this, they protect the vast majority of those who receive the money from hardship or poverty. Hardship and poverty whose side-effects include poor health often linked to poor diet, poor education outcomes for children, anti-social behaviour, and other negative effects which end up costing us all dearly.

So, if you’ve read and understood what I’ve written so far, “benefits” pay for themselves. They’re not a “drain” or “burden”. They’re the most effective way for a government to put oil into the economic engine, to put fertiliser on the economic farmers’ fields. (You’d think that a government that harps on about “growth” being the saviour might grasp the vital importance of that, but it seems not.)

Note:

Not about welfare benefits, but relevant to the idea that a healthy economy depends on the ability of people (“consumers”) to actually spend money on goods and services: here’s a blog post from Richard Murphy on how wages-often presented as a burden or cost to businesses- are in fact a very important part of demand, on which an economy like ours depends. Louis Vuitton handbags (or whatever it is they make) will never create prosperity alone.

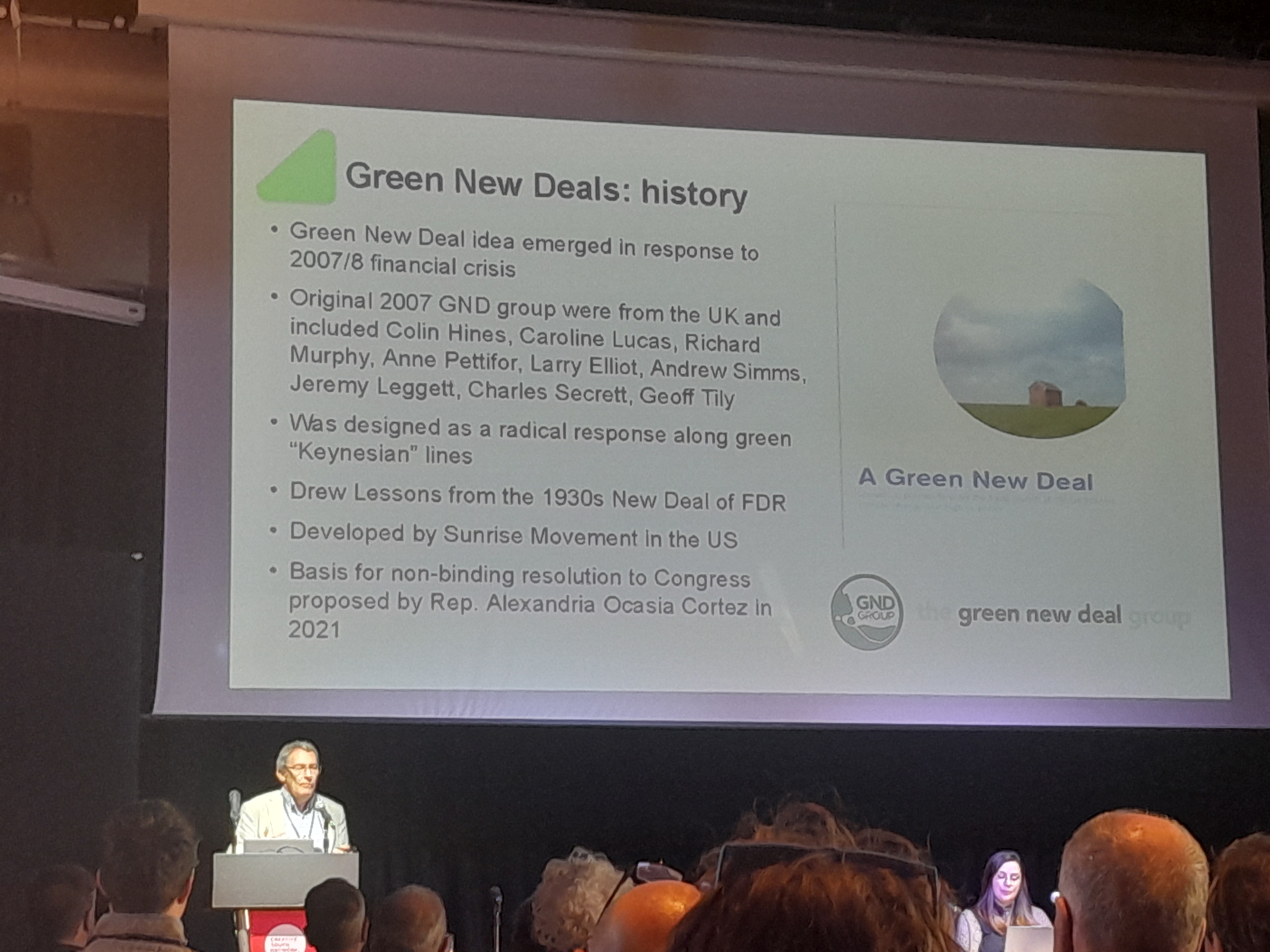

“Changing the conversation around money and the economy in the UK”

On Friday 12th September, Modern Money Lab UK held an anti-austerity Conference over two days at The Station, Bristol, to explore how the modern understanding of the government money and fiscal system (Modern Monetary Theory, MMT) gives a strong perspective on various policy issues. Modern Money Lab is an international educational non-profit organisation, which organises this conference and workshops in Sheffield, Vienna and Amsterdam. Their aim is “Changing the conversation around money and the economy in the UK”. I got on the bus and showed up.

“FINDING THE MONEY”

First was a showing of Marien Poitras’ film ‘Finding the Money’, which is fairly described as “An intrepid group of economists is on a mission to flip our understanding of the national debt — and the nature of money — upside down. This film will change your perspective on how countries around the world can tackle the biggest challenges of the 21st century: from climate change to inequality.”

Not just talking heads, the film uses lots of video clips, archive film and photos, sketches etc to explain the development of MMT from a historical point of view. It includes an explanation of what money really is- not a means of barter, as once taught, not a thing of intrinsic value, but a record of credit and debt. As Prof Randy Wray says, “There is no such thing as money without debt”. It goes on to look at the real nature of Government Bonds (“Bonds are interest-bearing currency”); and why government “borrowing” is really no such thing, in the way we understand borrowing in everyday life. It counters certain false allegations against MMT, such as allegations that MMT says “deficits don’t matter”- as Stephanie Kelton says in the film “Deficits do matter- they can be too big or too small”. And, how Markets (so often referred to in awe by the politicos and media) interact with how money policy really works- “markets only developed AFTER money”. How the expenditures of governments are primary, and markets secondary. Also, a look at how inflation can be managed in relation to government investment, interest rates, demand management, (for example how inflationary pressures were successfully controlled during WWII).

I’ve just given a brief picture of what the film covers, but you can watch it via this link . I promise you won’t be disappointed. The main speaker is Professor Stephanie Kelton (SK) who always talks engagingly and very comprehensibly.

Session 2- Austerity as a Political Choice: Associate Professor Steven Hail (Director, Economics of Sustainability Graduate Program, Torrens University and founder of Modern Money Lab)

Followed by- Resourcing a Greener New Deal, with Professor Kelton. After these presentations, there was a wonderful opportunity for a live Q&A with Stephanie Kelton via a virtual link.

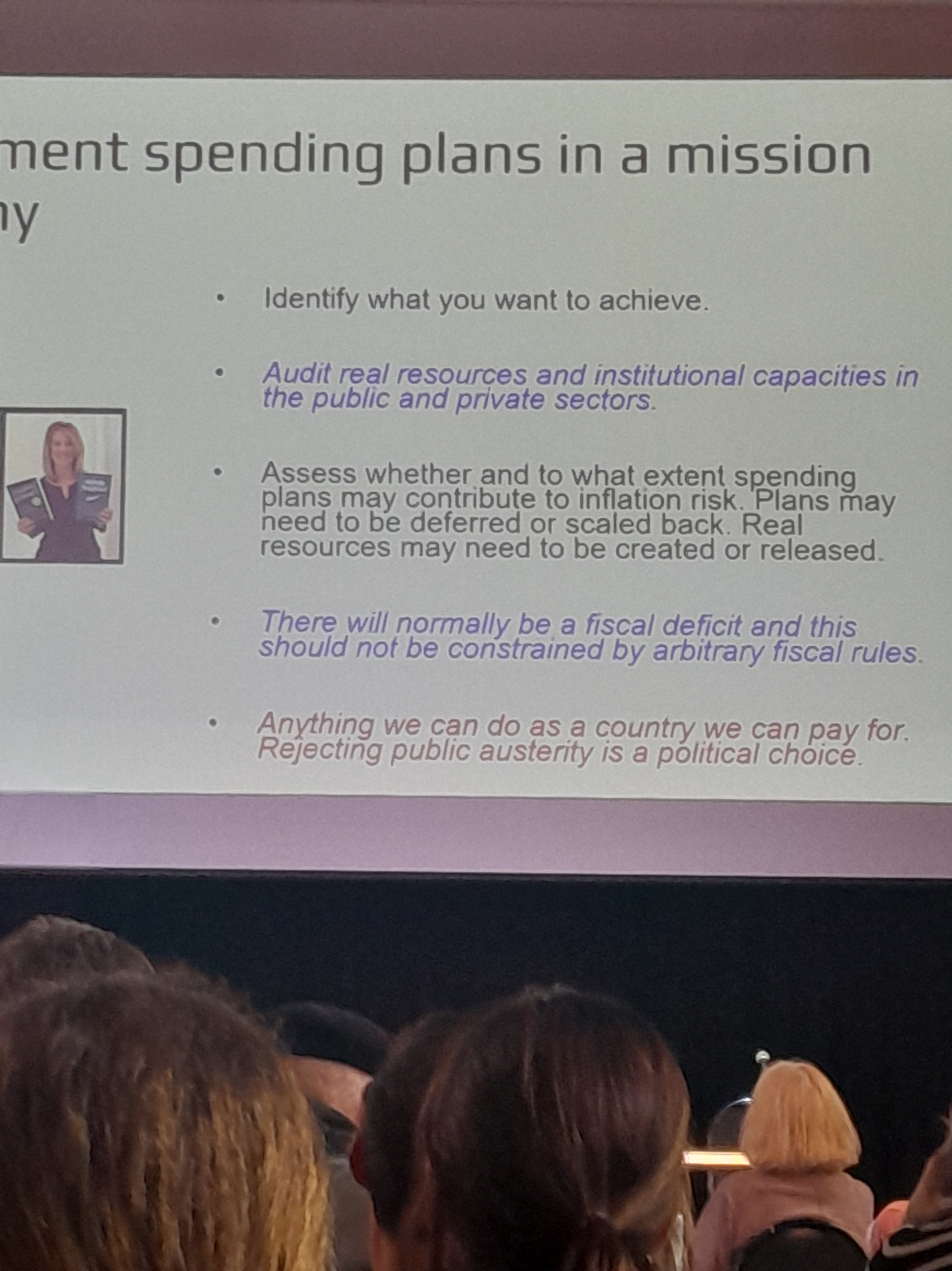

Topics covered included how policy to produce a better outcome for people and society has been done before (it’s not something new) in the Post-War period, using the guidance or perspective provided by J.M.Keynes; Why the Liz Truss budget was a crisis-the real reasons; how the neoliberal media and pressure groups try to frighten the people about fiscal policies by throwing out huge, often fictitious numbers (“meganumophobia”); the resource planning that is of primary importance before government investment takes place.

The Political Economy of the UK – moderated panel discussion

A panel session analysing the political economy of the UK, with a focus on the unnecessary damage from decades of austerity. Chaired by Randeep Ramesh (chief leader writer at The Guardian), alongside Plaid Cymru Councillor Mark Hooper, Sasha Josette (co-director of the Working Class Climate Alliance and long-time organiser and strategist) and Zack Polanski (leader of the Green Party and elected member of the London Assembly).

Outstanding moderation by Randeep Ramesh gave an opportunity for a fascinating discussion, including Zack Polanski demonstrating a deep understanding of the real nature of fiscal policy as it affects policy, with a very shrewd grasp of how this can be effectively applied. Including the concept of “Throughtopia”, the focus on desired outcomes in order to identify policy choices.

SATURDAY

What a Greener New Deal and wellbeing economy would look like in the UK: Professor Tim Foxon (University of Sussex), with response from Emma River-Roberts (Goldsmiths University)

Tackling health inequality in the UK: enabling people to live healthier lives, and rebuilding an NHS and care system that works for everyone. Chaired by William Thomson from Scotonomics, alongside Dr. Jaideep Pandit (professor of Anaesthesia at the University of Oxford) and Emma Hughes (Just Treatment). Example-Willie Thomson pointing out that 300,000 excess deaths between 2010 and 2015 could be attributed to austerity policy.

The UK’s housing affordability crisis: what can be done? Chaired by Sheridan Kates (Modern Money Lab UK and Green Party activist), alongside Sam Kidel (Head Organiser for Bristol, ACORN) and Simon Ripton (Derbyshire Dales Labour District Councillor, former Director Notts & Lincs Credit Union). Example– how fiscal rules in this area are deeply flawed because they ignore the asset side of the balance, i.e. the homes created.

A good job for everyone who wants one: ensuring full employment in the UK through a government job guarantee. Chaired by Phil Armstrong (Association for Heterodox Economics member and teacher), alongside Geoff Tily (Senior Economist, Trades Union Congress), Patricia Pino (PhD candidate at UCL Institute for Innovation and Public Purpose and cohost of the MMT Podcast) and Steve Laughton (former trade unionist, and author of upcoming book The Money Sham). Examples– Keynes: “If you look after employment, the Budget will look after itself”. Phil Armstrong reminded us that on a desert island, money is of no use, only the actual resources of food, water, shelter, materials- a principle which also applies to our modern society, which has the ability to generate Pounds Sterling easily, but only with due regard to resources.

VENUE

The Station was the former Central Bristol Fire Station, now a community hub mainly housing the Creative Youth Network. The tall doors (high enough for fire engines to enter and exit) have been given effective secondary glazing to almost silence the roar of traffic to the front, and you can see the former ladder-training tower in the yard to the rear.

AUDIENCE

There was a strong attendance, sold out at the venue on the Friday, plus online attendance. Attendees were of a wide range of ages, from student-y to a handful of likely-septuagenarians like myself. Some were new to the lens of modern monetary understanding, but seemed to be very interested. General enthusiasm was high, and one of the panel speakers declared that once the conditioning of the last 45 years is overcome, there is a very fertile ground out there in society for a different approach. to economic public policy.

Notes: 1. photos-Modern Money Lab, or my own(the poorer quality!) 2. You can read my introduction to Stephanie Kelton’s ground-breaking booK HERE

Why “taxpayers-money” is actually a smokescreen, designed and endlessly reinforced, to persuade ordinary people to accept policies which only serve the ultra-rich.

If you’d like to read my original post from 2019, it’s here.

We are all used to hearing about the “National Debt”, aren’t we. Politicians, newsreaders, pundits, quoting some scarily huge figure, that sounds a bit worrying, because we all know about personal debt in our own daily lives.

In fact, when you understand what the “National Debt” actually is, it’s not really anything to worry about- it’s actually something which benefits us as a society, by underpinning our whole economy. (And other benefits). And no, it doesn’t have to be “paid back” (like our own debt), either now, or by our children and grandchildren. Read on to find out why.

This post is reproduced from Professor-of-Accountancy Richard Murphy’s blog. It’s in plain English, little jargon, easy to read and understand. ( Only one chart, which you can skip if you find charts more confusing than helpful). It is a longish read, but well worth it.

Or, if you prefer videos to text, try this shorter, seven-minute one from him. It’s clear and absolutely straightforward, easy to follow.

“

RM: “We have just had another week when the media has obsessed about what they call the UK’s national debt. There has been wringing of hands. The handcart in which we will all go to hell has been oiled. And none of this is necessary. So this is a thread on what you really need to know.”

Where did the National Debt come from?

First, once upon a time there was no such thing as the national debt. That started in 1694. And it ended [in that form] in 1971. During that period either directly or indirectly the value of the pound was linked to the value of gold. And since gold is in short supply, so could money be.

Then in 1971 President Nixon in the USA took the dollar off the gold standard, and after that there was no link at all between the value of the pound in the UK and anything physical at all. Notes, coins and, most importantly, bank balances all just became promises to pay.

How is Government money created?

A currency like ours that is just a promise to pay is called a fiat currency. That means that nothing gives it value, except someone’s promise. And the only promise we really trust is the government’s.

If you don’t believe that it’s the government’s promise to pay that gives money its value, just recall when Northern Rock failed in 2007. There was the first run on a bank in the UK for 160 years. But the moment the government said it would pay everyone that crisis was over.

There’s a paradox here. We trust the government’s promise, which implies it has lots of money, and we get paranoid about the national debt, which suggests the government has no money. Both of those things can’t be right, unless there’s something pretty odd about the government.

And of course there is something really odd about the government when it comes to money. And that is that the government both creates our currency by making it the only legal tender in our country and also actually creates a lot of the money that we use in our economy.

How it makes notes and coin is easy to understand. They’re minted, or printed, and it’s illegal for anyone else to do that. But notes and coin are only a very small part of the money supply – a few percent at most. The rest of the money that we use is made up of bank balances.

The government also makes a significant part of our electronic money now. The commercial banks make the rest, but only with the permission of the government, so in fact the government is really responsible for all our money supply.

This electronic money is all made the same way. A person asks for a loan from a bank. The bank agrees to grant it. They put the loan balance in two accounts. The borrower can spend what’s been put in their current account. They agree to repay the balance on the loan account.That is literally how all money is made. One lender, the bank. One borrower, the customer. And two promises to pay. The bank promises to make payment to whomsoever the customer instructs. The customer promises to repay the loan. And those promises make new money, out of thin air.

What is the magic money tree?

If you have ever wondered what the magic money tree is, I have just explained it. It is quite literally the ability of a bank and their customer to make this new money out of thin air by simply making mutual promises to pay.The problem with the magic money tree is that creating money is so simple that we find it really hard to understand. We can have as much money as there are good promises to pay to be made. It’s as basic as that. The magic money tree really exists, and thrives on promises.

But there’s a problem. Bankers, economists and politicians would really rather that you did not know that money really isn’t scarce. After all, if you knew money is created out of thin air, and costlessly, why would you be willing to pay for it?What is more, if you knew that it was your promise to pay that was at least as important as the bank’s in this money creation process then wouldn’t you, once more, be rather annoyed at the song and dance they make about ever letting you get your hands on the stuff?

The biggest reason why money is so hard to understand is that it has not paid ‘the money people’ to tell you just how money works. They have made good money out of you believing that money is scarce so that you have to pay top dollar for it. So they keep you in the dark.

There are two more things to know about money before going back to the national debt. The first is that just as loans create money, so does repaying loans destroy money. Once the promise to pay is fulfilled then the money has gone. Literally, it disappears. The ledger is clean.

People find this hard because they confuse money with notes and coin. Except that’s not true. In a very real sense they’re not money. They’re just a reusable record of money, like recyclable IOUs. They can clear one debt, and then they can be used to record, or repay a new one.

The fact is that unless someone’s owed something then a note or coin is worthless. They only get value when used to clear the debt we owe someone. And the person who gets the note or coin only accepts them because they can use them to clear a debt to someone else.

So even notes and coin money are all about debt. They’re only of value if they clear a debt. And we know that. When a new note comes out we want to get rid of the old type because they no longer clear debt: they’re worthless. When the ability to pay debt’s gone, so has the value.

So debt repayment cancels money. And all commercial bank created money is of this sort, because every bank, rather annoyingly, demands repayment of the loans that it makes. Except one, that is. And that exception is the Bank of England.

What is different about the Bank of England?

So what is special about the Bank of England? Let’s ignore its ancient history from when it began in 1694, for now. Instead you need to be aware that it’s been wholly owned by the UK government since 1946. So, to be blunt, it’s just a part of the government.

Please remember this and ignore the game the government and The Bank of England have played since 1998. They have claimed the Bank of England is ‘independent’. I won’t use unparliamentary language to describe this myth. So let’s just stick to that word ‘myth’ to describe this.

To put it another way, the government and the Bank of England are about as independent of each other as Tesco plc, which is the Tesco parent company, and Tesco Stores Limited, which actually runs the supermarkets that use that name. In other words, they’re not independent at all.

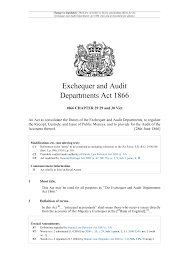

And this matters, because what it means is that the government owns its own bank. And what is more, it’s that bank which prints all banknotes, and declares them legal tender. But even more important is something called the Exchequer and Audit Departments Act of 1866.

This Act might sound obscure, but under its terms the Bank of England has, by law, to make any payment the government instructs it to do. In other words, the government isn’t like us. We ask for bank loans but the government can tell its own bank to create one, whenever it wants.

And this is really important. Whenever the government wants to spend it can. Unlike all the rest of us it doesn’t have to check whether there is money in the bank first. It knows that legally its own Bank of England must pay when told to do so. It cannot refuse. The law says so.

As ever, politicians, economists and others like to claim that this is not the case. They pretend that the government is like us, and has to raise tax (which is its income) or borrow before it can spend. But that’s not the case because the government has its own bank.

It’s the fact that the government has its own bank that creates the national currency that proves that it is nothing like a household, and that all the stories that it is constrained by its ability to tax and borrow are simply untrue. The government is nothing like a household.

In fact, the government is the opposite of a household. A household has to get hold of money from income or borrowing before it can spend. But the gov’t doesn’t. Because it creates the money we use there would be no money for it to tax or borrow unless it made that money first.

So, to be able to tax the government has to spend the money that will be used to pay the tax into existence, or no one would have the means to pay their tax if it was only payable in government created money, as is the case.

That means the government literally can’t tax before it spends. It has to spend first. Which is why that Act of 1866 exists. The government knows spending always comes before tax, so it had to make it illegal for the Bank of England to ever refuse its demand that payment be made.

Why do we have taxes?

So why tax? At one time it was to get gold back. Kings didn’t want to give it away forever. But since gold is no longer the issue the explanation is different. Now the main reason to tax is to control inflation which would increase if the government kept spending without limit.

There is another reason to tax. That is that if people have to pay a large part of their incomes in tax using the currency the government creates then they have little choice but use that currency for all their dealing. That gives the government effective control of the economy.

Tax also does something else. By reducing what we can spend it restricts the size of the private sector economy to guarantee that the resources that we need for the collective good that the public sector delivers are available. Tax makes space for things like education.

And there is one other reason for tax. Because the government promises to accept its own money back in payment of tax – which overall is the biggest single bill most of us have – money has value.

It’s that promise to accept its own money back as tax payment that makes the government’s promise to pay within an economy rock solid. No one can deliver a better promise to pay than that in the UK. So we use government created money.

So, what has all this got to do with the national debt?

Well, quite a lot, to be candid. I have not taken you on a wild goose chase to avoid the issue of the national debt. I’ve tried to explain government made money so that you can understand the national debt.

What I hope I have shown so far is that the government has to spend to create the money that we need to keep the economy going, which it does every day, day in and day out through its spending on the NHS, education, benefits, pensions, defence and so on.

And then it has to tax to bring that money that it’s created back under its control to manage inflation and the economy, and to give money its value. But, by definition it can’t tax all the money it creates back. If it did then there would be no money left in the economy.

So, as a matter of fact a government like that of the UK that has its own currency and central bank has to run a deficit. It’s the only way it can keep the money supply going. Which is why almost all governments do run deficits in the modern era.

And please don’t quote Germany to me as an exception to this because it, of course, has not got its own currency. It uses the euro, and the eurozone as a whole runs a deficit, meaning that the rule still holds.

So, deficits are not something to worry about. Unless that is you really do not want the UK to have the money supply that keeps the economy going, and I suspect you’d rather we did have government money instead of some dodgy alternative.

What actually is the National Debt?

But what of the debt, which is basically the cumulative total of the deficits that the government runs? That debt has been growing since 1694, almost continuously, and pretty dramatically so over the last decade or so, when it has more than doubled. Is that an issue?

The answer is that it is not. This debt is just money that the government has created that it has decided not to tax back because it is still of use in the economy. That is all that the national debt is.

Think of the national debt this way: it’s just the future taxable income of the government that it has decided not to claim, as yet. But it could, whenever it wants.

That’s one of the weird things about this supposed national debt. When we’re in debt we can’t suddenly decide that we will cancel the debt by simply reclaiming the money that makes it up for our own use. But the government can do just that, whenever it wants.

This gives the clue as to another weird thing about this supposed national debt. It really isn’t debt at all. Yes, you read that right. The national debt isn’t debt at all.

That’s because, as is apparent from the description I have given, the so-called national debt is just made up of money that the government has spent into the economy of our country that it has, for its own good reasons, decided to not to tax back as yet.

So, the national debt is just government created money. That is all it is. But the truth is that the people of this country did not, back in 1694 when interest rates were much higher than they are now, like holding this government created money on which no interest was paid.

You have to remember something else about those who held this government created money in times of old (though not much has changed now). They were the rich. If you don’t believe me go and read Jane Austen’s ‘Pride and Prejudice’ and note how much Bingley had in 4% government bonds.

And there was something about the rich, then and now. They get the ear of government. And so their protests about ending up with government money without interest being paid were heard. And so, money it might be, but from the outset the national debt had interest paid on it.

The so-called national debt still has interest paid on it. But then so do bank deposit accounts. And they look pretty much like money too. Only, they’re not as secure (at least without a government guarantee in place) and so the government can pay less.

But let’s be clear what this means. The national debt is money that represents the savings of those rich or fortunate enough to have such things on which interest is paid by the government because it’s been persuaded to make that payment.

Let me also be clear about something else. Those savings are not in a very real sense voluntary. If the government decides to run a deficit – and that is what it does do – then someone else has to save. This is not by chance, it is an absolute accounting fact.

Where money is concerned for every deficit someone has to be in surplus. To be geeky for a moment, this is an issue determined by what are called the sectoral balances. There’s a government created chart on these here.

The chart makes it clear that when the government runs a big deficit – as it did, for example, in 2009 – then someone simply has to save. They have no choice. And what they save is government created money. Which is exactly what is also happening now. A growing deficit is always matched by savings.

Who is saving from the National Debt?What are the official figures?

So who is saving? I am deliberately using approximate numbers, because they can quite literally change by the day. But let’s start by noting that the most common figure for government debt was £2,100 billion in December 2020.

Of this sum, according to the government, £1,880 billion was government bonds, £207 billion was national savings accounts and the rest a hotch-potch of all sorts of offsetting numbers, like local authority borrowing. I don’t think they do their sums right, but let’s start there.

Except, these official figures are wrong. Why? Because at the end of December the Bank of England had used what is called the quantitative easing process to buy back about £800 billion of the government’s debt, with that figure scheduled to rise still further in 2021.

So let’s, taking QE into account, discuss what really makes up the national debt, starting with an acknowledgment that if the government owns around £800bn of its own bonds they cannot be part of the national debt because they are literally not owed to anyone.

Around £200 billion of the national debt is made up of National Savings & Investments accounts. That’s things like Premium Bonds, and the style of really safe savings accounts older people tend to appreciate.

Around £400 billion of the national debt is owned by foreign governments, which is good news. They do that because they want to hold sterling – our currency. And that’s because that helps them trade with the UK, which is massively to our advantage.

But what’s also the case is that that because of QE UK banks and building societies have around £800bn on deposit account with the Bank of England right now. This is important though- this is the government provided money that stops them failing in the event of a financial crisis.

And then there’s very roughly £700 billion of other debt if the Office for National Statistics have got their numbers right (which I doubt: they overstate this). Whatever the right figure, this debt is owned by UK pension funds, life assurance companies and others who want really secure savings.

Why do pension funds and life assurance companies want government debt? Because it’s always guaranteed to pay out. So it provides stability to back their promise to pay out to their customers, whether pensioners, or life assurance customers, or whoever.

So now I have explained how we get a national debt and that it’s a choice to have one made by government. I’ve also explained that all it represents is the savings of people. And I’ve explained the government could claim it back whenever it wants. And I’ve covered QE.

So do we need to worry about the national Debt?

So, the question is in that case, which bit of the national debt is so worrying? Do we not want people to save? Or, would we rather that they had riskier savings that our pensions at risk? Is that the reason why we want to repay the national debt?

Or do we want to stop foreign governments holding sterling to assist their trade, and ours?

Alternatively, do we want to take the government created money back out of the banking system when it’s saved it from collapse twice now (2009 and 2020), and which provides it with the stability that it needs to prevent a banking crash?

Or is the national debt paranoia really some weird dislike of Premium Bonds that suggests that they are going to bring the UK economy down?

The point is, once you understand the national debt it’s really not threatening at all. And what you begin to wonder is why so many people obsess about it. To which question there are three possible answers.

The first is that the obsessive do not understand the national debt. The second is that they do understand it, but want to make sure you don’t. And the third is that they realise that if you did understand the national debt there would be no reason for austerity.

Of these the last is by far the most likely. There’s always been a conspiracy to not tell the truth about money, and how easily it’s made. There’s also a conspiracy to not tell the truth about the fact government spending has to come before taxation, and the law guarantees it.

And I strongly suggest that the hullabaloo about the national debt – which is a great thing that there is absolutely no need to repay and which is really cheap to run – is all a conspiracy too.

The truth is that the national debt is our money supply. It keeps the economy of our country going. It keeps our banks stable. And it also represents the safest form of savings, which people want to buy.

There is no debt crisis. Nor is the national debt a burden on our grandchildren. Instead, the lucky ones might inherit a part of it.

But some politicians do not want you to know that there is no real constraint on you having the government and the public services you want. What the government’s ability to make money, sensibly used, proves is we do not need austerity. And we never did.

Instead, the opportunity we want is available. And we do not need the private sector to deliver it. The government can and should take part in that process as well, which it can do using the money it can create as the capital it needs to do so.

But in order to pursue their own private gains and profits some would rather that this is not known, so they promote the idea that money is in short supply and that the national debt is a danger. Neither is true. We need to leave those myths behind. Our future depends on doing so.

My notes:

Richard Murphy is a Chartered Accountant and Emeritus Professor of Accountancy. The words are his. I have only re-arranged a little, added some pictures, used bold to pick out some points, edited lightly for clarity, and broken it up into sections with some “reader questions” (in bold italics). Reproduced with permission. To read the original blog post, it’s here, with some interesting comments from his readers. There’s a lot of misunderstanding of government debt,( much of it deliberately drummed into us for political reasons), so I hope this will help you get a whole new understanding. I would love to hear from you how you got on with it. You can write to me via thepoundinyourpocket@gmx.com if you wish. Or comment on the blog post if you have questions.

My own earlier pieces on National debt on this blog are here and here.

It was just after midnight on MPC-Meeting-Eve in the upmarket-suburban houses of Bank of England Governor Andrew Bailey, and Chief Economist Huw Pill. They were woken from fitful, fretful, dozing slumber by three ghostly, shadowy figures.

The first announced himself as The Ghost of MPC-Eve Past. He took them to 1942, when there were desperate shortages of everything people needed or wanted. There was the potential for runaway price-inflation. But there was none, because rather than raising Bank Rate, the government imposed strict price controls, so that manufacturers and suppliers were unable to rake in great profits by raising what they charged for all these goods and services .

The second, the Ghost of MPC-Eve Present, took them on a lightning tour of small business proprietors, crippled by steeply-rising finance costs and unaffordable business costs. And ordinary families, terrified by £400 per month increases in their mortgage payments, on top of inflated food and energy costs. Elswhere, holders of major financial assets were receiving gratifyingly substantial extra income.

The third, the Ghost of MPC-Eve Yet to Come, showed them the future PhD theses and history books, which were less than complimentary about the actions of the leaders of the UK Central Bank, influenced by the UK Finance Ministry (The Treasury), which demanded successive interest rate rises to protect the asset-owners and rentiers of Britain against inflation. https://economicsfromthetopdown.com/2023/04/16/how-interest-rates-redistribute-income/

The next morning, chastened and contrite, they met for coffee, and composed the following letter to the Prime Minister and Permanent Secretary to the Treasury:

“Dear Prime Minster and Permanent Secretary,

In Confidence (for now).

Sorry, gentlemen, but we’re not prepared to go on doing your dirty work for you. You’ll just have to carry on screwing the economy and the population by yourselves.

We’ve given out all that crap about wage-rises being inflationary, and the mainstream media have faithfully regurgitated it, but too many people are reading the alternative-macroeconomics reports on social media, substacks, etc, which point out that the “wage-price-spiral “ is, to put it bluntly, a load of old cobblers. Even the IMF published a study last November looking at several economies over six decades, and couldn’t find any significant evidence for it. In fact, when price-inflation rises steeply, wages struggle to keep up.https://thenextrecession.files.wordpress.com/2022/11/wpiea2022221-print-pdf.pdf

And as for that nonsense about rate rises “damping down demand” to control inflation- well, that’s fooling very few when it’s obvious that most people are struggling to afford the basic essentials, when their wages are steadily falling in real terms. The average price of fish and chips at the chip shop has gone from about seven quid to nine/ten quid in about 12 months, but that ain’t because people are feeling flush and treating themselves more often.

The BBC, with the un-challenging Faisal Islam, and ITN, with the blathering Joel Hills, may not be rocking the boat, but even the Express’s report the morning after the last rate rise was furious. (Despite their geriatric readership fondly imagining that higher Bank Rate might translate into more interest being paid on their retirement savings, haha).

We might be able to get away with it a bit by admitting that a high Bank Rate helps to keep the Sterling exchange rate up when we are importing most essentials from abroad, but you haven’t let us say that, have you? And in any case, that’s not your priority, is it?

We’ve had enough, gentlemen. The rate-hike game is more-or-less up. You can sack us, but you will need to find people who understand how to run a Central Bank, so good luck with that. And it wouldn’t play well in the media, however much you spin it.

Very sincerely, Andrew and Huw.”

And they set off to hand-deliver their missives, remorsefully delivering gifts to foodbanks along the way.

Like a lot of popular myths about economics, the “wage-price-spiral” sounds so convincing. “Wage demands cause wages to rise, so suppliers have to put their prices up, so workers demand higher wages. So inflation runs riot, everyone suffers.”

Seems like common-sense? Well, it isn’t. It’s an outstanding example of the old Army saying, “bullshit baffles brains”. And, common-sense is all very well when crossing the road or dealing with scam emails, but it’s a lousy guide to macroeconomics.

Who’s talking about it? Here’s Andrew Bailey , reported talking to BBC’s R4, trying to justify the latest Bank Rate rise. You’d think, wouldn’t you, that the Governor of the Bank of England would know a thing or two about how the economy works? Highly educated fella, years of experience in that field, with a large staff of technical experts to supply him with data and analysis.

“Andrew Bailey told The Today Programme that policy makers must act to prevent a wage-price spiral from fuelling inflation, which is growing at its quickest pace in four decades and forecast to leap above 13% later this year.”

And: ““I’m not saying nobody gets a pay rise, don’t get me wrong. But what I am saying is, we do need to see restraint in pay bargaining, otherwise it will get out of control”.

But, when we look a little deeper into this, the picture looks very different. (For this post, I am indebted to “The wage-price spiral refuted” from Michael Roberts’ blog, November 2022. You can read it here with a link to the full IMF study).

The International Monetary Fund (IMF) has just published a study, a comprehensive data analysis, which examined episodes of wage and price rises in several countries since the 1960s. They were looking to see whether wage-price “spirals” did actually occur. And the answer is, usually not. Nein, Niet, Nej, not on your nelly. (And the IMF are the instrument of international financial orthodoxy, not some left-wing tribune!)

From the IMF conclusions:

“Wage-price spirals, at least defined as a sustained acceleration of prices and wages, are hard to find in the recent historical record.

Moreover, sustained wage-price acceleration is even harder to find when looking at episodes similar to today, where real wages have significantly fallen. In those cases,nominal wages tended to catch-up to inflation to partially recover real wage losses,

When focusing on episodes that mimic the recent pattern of falling real wages and tightening labor markets, declining inflation and nominal wage growth increases tended to follow – thus allowing real wages to catch up.“

Michael Roberts: “What does the IMF conclude? “We conclude that an acceleration of nominal wages should not necessarily be seen as a sign that a wage-price spiral is taking hold.” In inflationary episodes, wages just try to catch up with prices. But even then, wage rises do not cause wage price spirals”

He’s saying that when, as now, a load of prices rise rapidly owing to external and supply shocks-(shortages of transport, labour, materials, manufacturing capacity post-pandemic/ sanctions and export restrictions following the war in Ukraine) , then wages are not leading the price rises, but trying to catch up. The establishment likes to pretend that “excessive, greedy wage demands” are forcing wages up- but in reality, it’s workers (whose wages have mainly been held down since the GFC of 2009 or actually fallen) seeking to defend their standard of living, rarely improving it.

Michael Roberts again: “Despite this evidence refuting the wage-price spiral, mainstream economists and the official authorities continue to claim that this is the key risk to sustained inflation. The reason for doing so is not really because the economic prize-fighters for capitalism believe that wage rises cause inflation.

It is because they want ‘wage restraint’ in the face of spiralling inflation in order to protect and sustain profits. To this aim they support central bank interest rate hikes that will accelerate economies into a slump – coming in the next year.”

Now, we begin to see what’s going on here. If wages go up across the board, profits fall. So workers rather than companies are taking the bigger hit from inflation. So, “economists and the official authorities” –e.g. Andrew Bailey and the Monetary Policy Committee of the Bank of England- are leading us up the garden path. Why might they be doing that? Probably steered by HM Treasury/Government?

Michael Roberts again: “So the real aim of interest-rate hikes is not to stop a wage-price spiral but to raise unemployment and weaken the bargaining power of labour. “

He quotes Financial Times eminent columnist Martin Wolf: “Monetary policy must be tight enough to achieve this. In other words, it must create/preserve some slack in the labour market.” Translation– pushing up interest rates, which causes or deepens a recession in conjunction with government spending cuts, will cause increased unemployment, which will kill off wage demands. If workers fear for their jobs, they will reluctantly accept low wages and keep on struggling to survive. All this is in the context just now, of what the authorities call a “tight labour market”. (Post-pandemic, many older workers have left the job market, and Brexit combined with the pandemic has severely limited the availability of workers from abroad to fill the gap).

Profits are largely preserved, and for those companies supplying the essentials-gas, electricity, food, transport- they are in some cases driven up substantially.

This is not something new. Roberts quotes Alan Budd, who was chief economic advisor to Margaret Thatcher in the 1980s: ““There may have been people making the actual policy decisions… who never believed for a moment that this was the correct way to bring down inflation. They did, however, see that [monetarism] would be a very, very good way to raise unemployment, and raising unemployment was an extremely desirable way of reducing the strength of the working classes.” (“Monetarism” here means the myth that money is in short supply, and that government spending must be cut- this is not true for the UK, which has had the ability to issue pounds sterling as required by order to the Bank of England ever since the scrapping of the Gold Standard in 1973).

In summary: the “wage-price spiral” is a myth, and it’s being used to force wages down. After 12 years of stagnant growth, or falling in real terms . As Richard Murphy showshere.

I am grateful to Ian Tresman of MMT.works for editing suggestions.

Further reading: This Yahoo News report from August 2022 is good, and has some useful graphs and videos.

“Whichever party is in office, the Treasury is in power”- Harold Wilson (UK Prime Minister 1964-1970, 1974-1976)

Why is the Treasury, actually a government department, so powerful and prestigious? How much influence does it have on the policies of UK governments? And, has its influence been beneficial, or highly damaging in recent decades? Let’s have a look at this.

The Treasury is a department of UK government, but one which asserts control over the budgets of all other departments. In political terms, it’s the tail that wags the dog – because it has the prestige and expertise to influence decisions about what policies elected governments carry out, or their extent. It even does its own briefing to the media, who rarely challenge or ignore it.

““Within Government, the elite institution is HM Treasury….As such, it is the great magnet for the brightest and best in the public sector. Which means that it has been consistently arrogant and over-confident.” (Robert Peston)

Michael Cockerell’s 2012 documentary film “The Secret Treasury”, for the BBC series, “The Great Offices of State” (watch it on YouTube here), shows his ability to get access to important public servants and former Ministers of State, and hear them speak in remarkably clear and frank terms, is outstanding. I am grateful to him for much of the material in this post, although I do not necessarily agree with his conclusions.

What has been said about the Treasury?

Michael Cockerell: “In Whitehall, knowledge is power. And the great office which claims to know most of all is the Treasury”.

Ken Clark (former Chancellor) : “ …[the Treasury] it’s like an Oxbridge college, you know, brilliant minds, …and completely detached from the real world”.

Nigel Lawson (former Chancellor): “The core of the Treasury is its hostility to public spending”

A former Permanent Secretary: “all governments have to be restricted in what they can do, because there are only a limited number of resources available” (I suspect that he meant, by “resources”, money, Pounds Sterling, which in the orthodox economic dogma, is limited or constrained, under the household-budget narrative. Not, as we now know, actual resources of labour, materials, expertise, buildings, etc, which are the only real constraints for a sovereign-currency nation).

Or was he being deliberately ambiguous, leaving people to conclude that he meant money but secretly he knew the real constraint is real resources?

Later in the film, Cockerell refers to “eye-wateringly large sums of taxpayers money”, referring to the re-capitalisation of the banks after the GFC. We now know that “taxpayers money” is a fallacy, a myth politically very useful to Thatcher and her successors. To be fair to Cockerell, very few people understood the true nature of government finance in 2012 – I certainly didn’t. It is only since about 2017 that the MMT understanding of the reality of macroeconomics has gained substantial traction. Stephanie Kelton’s seminal 2019 book, “The Deficit Myth”, has been massively influential in the spreading of understanding beyond the inner circle of progressive economists and writers.

How influential has the Treasury been since, say, 1960? Prime Minister Harold Wilson found the Treasury obstructive, and set up the DEA (Dept of Economic Affairs, headed by George Brown, to counter-balance it.

“The idea behind Harold Wilson’s creation of the Department of Economic Affairs (DEA) in 1964 was to drive the economy towards sustainable growth amid the early signs of industrial decline, and much was made of the benefits of its ‘creative tension’ with the Treasury. The growth strategy was shattered by the adherence to the parity of sterling by Wilson and Jim Callaghan as Chancellor, and by the resultant Treasury-led cuts which were brought in to defend sterling.”

“The second episode occurred during the post-1974 government when Tony Benn led an attempt to develop the alternative economic strategy through the Department for Trade and Industry (DTI). This foundered partly due to the Treasury’s dominance of the economics agenda (and in particular, its central role in negotiating the IMF bailout”

(University of Sheffield Political Economy Research Unit, Nov 2018)

The IMF (International Monetary Fund) “bailout” was actually an utterly un-necessary nonsense, which was driven by the Treasury’s obsession with defending the Sterling exchange rate, and the Treasury were able to browbeat the Government into it. Now, we know that the UK currency needs to be free-floating, as it has been since the debacle of the ERM Black Wednesday. (More on this later). For good or ill, (often ill) the Treasury has been able to dominate government policy in economic terms. The Treasury’s website, in a graduate recruitment drive, says:

“Our specific priorities are:

Reducing the deficit and rebalancing the economy

Spending taxpayers’ money responsibly and ensuring value for money

Creating a simpler, fairer tax system – alongside a well-functioning welfare system”

And:

“HM Treasury is the government’s economic and finance ministry. We maintain control over public spending, decide how money is raised from taxpayers, set the direction of the UK’s economic policy and work to achieve strong and sustainable economic growth.”

So, the Treasury’s belief in its own power and superiority is demonstrated, along with its adherence to the false narratives of “taxpayers money”, and “reducing the deficit”. Both severely harmful to the UK economy, and society, from the perspective of the modern understanding of Government finance. (Modern Monetary Theory).

Let’s look at some events in the decades from 1979 to 2008, to examine what the role of the Treasury has been.

In addition to the IMF loan referred to earlier, there have often been tensions between Governments, and The Chancellor and Treasury; sometimes between the Chancellor and his Treasury. When the Conservatives won power in 1979 “Margaret Thatcher came to power determined to do battle with the Treasury. She was a passionate believer in Monetarism, and the power of the market. She saw the Treasury as stuffed full of Keynesians, who believed in the power of the State to run the economy” (Cockerell). Her devotion to Monetarist dogma, which we now realise was both fraudulent, and politically convenient (for governments run by, and favouring the establishment), became the dominant economic orthodoxy, and is still very powerful today. She promoted the two fallacies/myths of “taxpayers’ money” and the “household budget” (that governments must balance their books, like that of a household) very effectively. I suspect that she truly believed the myth. If you listen to her speeches and interviews of the time, her vehement conviction is clear, and noticeably expressed in a superior, condescending, and contemptuous manner: “Money’s just the same, if you print too much of it, its value will fall … bringing down the growth in the supply of money, steadily closer to the supply of goods and services…{Monetarism] is as essential as the Theory of Gravity, and you can’t avoid it, if you want to tackle inflation.”

To this end, as Michael Cockerell says: “She appointed…Geoffrey Howe as her first chancellor, to lead a team of Monetarists. “(1979-81)

Lord Kerr, a former Treasury Permanent Secretary: “{the Treasury] was basically a Keynesian institution”. (How ironic that sounds now).

What followed? Sir Steve Robson, 2nd Permanent secretary to the Treasury: “Geoffrey Howe came in and said, ‘I want to have an early cut in public spending’” The cuts to public spending followed, with the highly damaging results we would now expect, from our modern perspective. As Michael Cockerell says, “Howe’s first Monetarist Budget was so restrictive, it plunged the ailing economy into recession, And two years later, he further alienated Keynesians in the Treasury, by slashing public spending in the teeth of a recession”

“in 1981 there were riots across the country as Mrs Thatcher’s Monetarist medicine took effect. The economy imploded. 15% of manufacturing industry disappeared, as bankruptcies and unemployment reached record levels. It was only when Mrs Thatcher … by demolishing the Argentinian invaders of the Falklands, that her fortunes changed. As Britain came out of the recession, she won a landslide victory. She was determined to continue with her transformation of the Treasury [to Monetarism] and brought in another true Monetarist disciple, Nigel Lawson. At the Treasury, Monetarist mandarins were beginning to replace the Keynesians. But soon things began to go wrong between the Treasury and Number 10.”

Despite being a Monetarist, Lawson became uncomfortable. Cockerell: [slight paraphrase] Alan Walters was Mrs Thatcher’s economic advisor. Nigel Lawson felt he undermined the City’s trust in the Chancellor and demanded Thatcher sack Walters. She accused him (Lawson) via the Press of having created the inflation.” Thatcher refused to sack Walters, and Lawson resigned.

Gus O’Donnell, the distinguished former Cabinet Secretary, takes up the story: “when you get big policy differences between a chancellor and the Prime Minister, it’s very dangerous for Governments [which led to] a change of Prime Minister to John Major … who [appointed] Norman Lamont. Major accepted the Treasury’s argument that Britain should join the ERM.”

This takes us to another huge event for the UK economy, and the Treasury: the ERM debacle, and Black Wednesday. As in the IMF loan episode, false understanding of the reality of a fiat-currency economy and the need for floating exchange rates, led to a disastrous event, and some disgrace for the Treasury. (See also Note 1.)

Cockerell: “the govt had to convince the markets that it would resolutely defend the value of the pound … Black Wednesday [followed], interest rates raised to 15% in an attempt to defend parity”.

Peter Hennessey, London University: “the Treasury have often looked abroad to impose discipline of unruly spending departments … a nation that has an appetite for consuming more than it earns”.

Cockerell: “… the Treasury was very battered. Very battered after the IMF deal was scrapped.” The IMF Loan madness (a sovereign currency nation should never need a loan from any international body, as it can issue its own currency as much as needed), and the ERM debacle, have two things in common: The Treasury’s wrong-headed belief in the importance of the currency’s exchange rate. Today, a floating exchange rate is now accepted as normal and natural.

We can now move on to the third major economic event of the period since 1964, the 2008 Global Financial Crash (GFC). Before this, in 1997, George Brown took over as Chancellor of the Exchequer, and the “economy had grown healthier after Black Wednesday” (Cockerell, ibid). His economic advisor was a youthful Ed Balls. Their obsession was to convince that the Labour Govt was “financially responsible”, and to that end Brown gave operational responsibility for interest rate setting to the Bank of England. (To this day, many people are still convinced that the Bank of England is actually an independent body, not a wholly owned subsidiary of the UK State). Brown and (PM) Blair’s relationship deteriorated over the next several years, Brown operated with just a small team of close advisors, and if Treasury officials disagreed, they were sidelined or “shunted out”. Brown steadily built up the Treasury’s already dominant position in Whitehall, seeking to be dominant in social policy, as well as economics. Brown regarded Blair as very prone to leaking to the Press, so kept his policy operations/ budget plans secret from Number 10. At one point, Blair by-passed Brown and the Treasury to announce on TV a decision to increase heavily health service spending. Brown was furious.

Brown took a “hands-off” approach to financial sector regulation- huge tax receipts were coming in from it. Also, “Brown took the brakes off public spending, as Britain shared in a global economic boom.” (Cockerell).

When Brown succeeded Blair as PM, he chose a successor, close ally Alastair Darling, so that the antagonism between Number 10 under Blair, and Number 11, did not recur. But the consequences of deregulation of the financial sector soon caused storm clouds to gather. In August 2008, Darling announced a “60-year low” for the economy. The banking bubble had burst. Northern Rock had collapsed, followed by Lehman Bros. “RBS had lent billions against toxic assets” (Cockerell). Darling said the Treasury were not prepared, did not foresee it.

“Treasury and Number 10 put together a plan to bail-out the banks” (Cockerell), “treasury officials didn’t go home for days” (Darling). The Tories, following the Thatcher “handbag economics” model, portrayed a huge burden of debt, the “greatest debt burden in our history”, claiming falsely that “The Treasury would now have to balance the books”. Sir Steve Robson regarded it as a failure, with “debt getting too big”. Brown, to his credit, understood the power of the Bank of England, on the order of the Treasury, to re-finance the banks, and issue credit-swaps (called “quantitative easing”), to stabilise the economy. Which had the unwelcome side-effect of inflating capital assets for the owners of wealth.

To return to my questions at the start of this piece: “How much influence does [the Treasury] have on the policies of UK governments? The influence of the Treasury was significant over the IMF loan of 1974, and the ERM catastrophe, both involving an unwise adherence to maintaining a desired exchange rate. In both cases, the governments involved were persuaded to take a disastrous course of action. But it seems that Margaret Thatcher’s push to cut public spending was against Treasury (Keynesian) instincts and led to the Treasury being dominated by Monetarists. This must have helped the pressure to restrict spending on public services, which caused much harm over the following decades, and reached its nadir in the Austerity policies which dominated post-2010.

And, has its influence been beneficial, or highly damaging in recent decades?

Although the Treasury was regarded by Thatcher as “Keynesian”, too keen to spend public funds, it has been mainly Monetarist in doctrine since then, and resistant to spending on public services generally. Its influence in restricting spending by departments on public services has been harmful, to the economy and society. Thatcher’s Monetarist dogma: cut-public-spending, devotion to “the market” (which ignores the essentially rigged nature of markets), and the pretence that taxes fund spending,is still very strong today, both in political discourse and the mainstream media. (Even, sadly, in the more left-leaning policy offerings).

Surely, following the enormous level of spending necessitated by the Covid response, the reality of currency-issuance by the Bank of England, unrelated to taxation, should be obvious? Despite the usual misleading dressing-up as “borrowing”, I find it hard to believe that the top layer of Treasury officials do not understand this reality, so it follows that their department doesn’t want to rock the boat, so continues to mislead.

In his thoughtful book ‘WTF?’ (Hodder & Stoughton, 2017), highly-experienced journalist Robert Peston says “The propensity of the of the British economy to swing from relatively extreme boom to bust, is equally down to the Treasury’s obsession with prioritising the control of inflation…and its rejection of taxing and spending as active levers of employment creation and growth management.”

He goes on to describe (very fairly, in light of what this article has described above, the Treasury as “an elite institution both too big for its boots, and too powerful for the country’s needs; too closed to arguments on the questions that determine our prosperity.”

Any future Government committed to seriously progressive economic and social policies, will certainly have to be prepared to impose their will on a Department which is powerful because of its expertise in the details, the nuts and bolts, of state financial management. Peston (ibid) recommends that the Cabinet Office be restructured and empowered to to take control of economic policy away from the Treasury (rather reminiscent of George Brown’s DEA in 1964?), and “should make its priority restoring dignity, security and rising living standards for those on average and lower incomes.”

Note 1. re The ERM/Black Wednesday: Professor Bill Mitchell has written this explanation here:

“The problem then was that the British government had foolishly joined the ERM (a fixed exchange rate system with European nations) and the structural differences between the different nations meant that the system was unsustainable.

The financial markets surmised (correctly) that the system would eventually be unsustainable and Britain would have to leave and float.

They also guessed correctly that the British government would stubbornly try to stay in the ERM as a result of ideological biases within the top echelons of the Cabinet.

Germany was also causally implicated because the Bundesbank refused to help its currency partners through interest rate settings and foreign exchange market interventions.

So the currency was ripe for financial market trades (short selling) and ultimately as long as the Government tried to defend the indefensible (the fixed exchange rate membership of the ERM), these trades would be successful and the currency would fall significantly in value.

The currency stability ended when Britain left the ERM, which is what MMT would have predicted.

Then, the problem was the fixed exchange rate obsession, which was never sustainable and that vulnerability was exploited.”

All material quoted from the BBC film “The Secret Treasury” 2012 is copyright BBC UK, and is reproduced by kind permission.

I am grateful to Malcolm Reavell, Nigel Hargreaves, for their help in preparing this article; and to David Vigar for advice on copyright. It is intended as a discussion piece, and comments are welcome.

This is a guest post. In it, Professor Richard Murphy(read his excellent blog here) explains very clearly everything you need to know about how money is created by governments. And why it’s important for all of us to understand it. Longer than most of the posts in this blog, but all in plain, clear language. No jargon, diagrams, graphs, or anything you need a degree in economics to understand. My notes in italics, and I have highlighted some parts in Bold for reading convenience.

“Very few people seem to understand how money is created. Mainly that’s because when they’re told, it seems so simple that they can’t believe something that’s so important that we’re willing to pay a lot to get it, is created so easily. This thread explains how money is created.

What this thread also explains is that if we understand money we can completely reimagine how the economy really works, which is the pathway to rebuilding from the mess we are in. Which makes this a pretty big deal. I make no apology for its length as a result.”

Let’s start at the very beginning. A person goes into a bank and asks for a £1,000 loan. The bank checks them out, and agrees. And that is all that it takes to create new money. Money is just a promise to pay. That simple exchange of promises is all it takes to create it.

Most people think there must be something that backs up the value of money. Gold, most likely. But there isn’t. Money is just a promise to pay, and has been for almost 50 years now. Mutual promises to pay creates all the money we have.

So in the example of that £1,000 loan, the customer promises to pay the bank. So the bank opens a loan account for them. That records their promise to repay. And the bank puts £1,000 in the customer’s current account. They promise to let the customer spend that how they want.

Two promises. Two accounts. And as a result we get new money. That is how all money is created. It is as simple as that.

There is no one else’s money involved in this process. The bank does not lend out the money saved with them. And there are no notes and coin moved from one pile to another pile to back this all up either. There are just two promises. And then there is new money.

Making money really is as simple as promising to repay it. So why is it so expensive for some people to get hold of it? That’s not because the money itself is expensive. Clearly, it isn’t. That’s because there’s a risk that they will break their promise.

But the government borrows more cheaply than anyone else. It creates the currency – the pound – and declares it legal tender. And it has its own bank – the Bank of England. This means the government can lend to itself. So it can never run out of money. It is risk free.

The rest of us don’t have a bank, and can’t declare the money we make to be legal tender. So all other lending is riskier. Including the money that you lend to your bank, which is exactly what you are doing if you have a bank account that’s in credit.

If you think you have ‘money in the bank’, think again. You have not. You just have a promise from the bank to pay you money if you demand it. And if they can pay it, of course. You’re now the banker. They’re the borrower. And you have the risk they won’t repay.

And that risk is real. Remember Northern Rock? The government stepped in. This is why all bank deposits in the UK have to be guaranteed by the government to a limit of £85,000. If they weren’t it’s likely no one would trust the banks to repay.

But what this means is that for most people (not the wealthiest, and not big business) the government guarantees all the money that we have. And it even, by implication, guarantees that the banks exist so that they are there to lend if and when we require it.

How is it possible that although all money is made by promises – including yours, and mine – the government is so important? First, it alone creates the currency. Secondly, as I noted, it has its own bank. So it can always repay, because it will always lend it money.

So, it’s the government and its Bank of England, and their promise to pay that is actually behind the real value of our money. Not gold. Not notes. Not coins. Not how strong the rest of the UK banking system is. The promise that the government makes is what matters.

But why is its promise so good? Because it has the means to back it up. Having a bank is not enough. Having the means to tax changes everything. That, and the ability to pass law to make sure tax is paid. And then only in the currency the government chooses – the pound.

Tax is what gives the pound its value. If the government could just create money without limit it would soon be worthless. But it does not do that. Tax ensures that the government can control the amount of money in the economy.

A lot of that money is created by the government. Every time it spends it tells the Bank of England to pay whoever is required. And it does that, because it trusts the promise the government makes to repay it. Well it would, wouldn’t it? After all, the government owns it.

But what the Bank of England does not do is check whether it’s got money available to lend the government to spend. It does not need to do so, after all. All it need do is trust the government’s promise to repay. And then it creates the money that the government wants to spend.

This is really important though. What it means is that tax does not need to be collected before the government spends. Instead the government always spends the money its bank creates for it, when instructed to do so.

But that means something else. It means the government never spends taxpayers’ money.

It also means that tax does not fund spending. That can happen without tax.

So what does tax do? It does something really important. It recovers the money the government has spent into the economy. Enough has to be collected to control inflation and make good on the promise that the government gives when it guarantees all our money.

Does that mean the government has to balance its books? No way does it mean that. Controlling inflation is the goal, and what we’ve learned is we can run deficits, and control inflation.

But that has come at a price. That’s been unemployment, low wages and lots of crap jobs that add little value to society or the lives of those who do them. To be polite, that’s the economic policy of a callous government that does not care.

Forcing people into meaningless, low paid work is a price too high to control inflation, even if that also means lower taxes and that deficits do not threaten to create economic instability. There has to be a better way to manage the value of money than this.

And there is. We could have a government promise full employment. It could create the jobs we need. It could force up the minimum wage by guaranteeing local work for anyone who wanted it. And we could improve benefits too. All using government made money. Not tax.

But would there be inflation then? Not if we then taxed enough and cut spending a bit. But people at work in good jobs do pay more tax. And they claim fewer benefits. So that condition is easy to meet. And if we still needed more tax? Well, we could do that, if needed.

But that need would not be to fund the spend. Tax is never needed to fund spending. Always remember that. It’s needed to control inflation. And to redistribute income and wealth, and other social reasons. But not to fund spending. Ever. Money does that.

So, I hear you say, why do governments borrow then? After all, if they can create all the money that they need why do they have to borrow other people’s money? Doesn’t the fact that they borrow prove me wrong? No, it doesn’t. Because they don’t need to borrow.

The government did have to borrow when money was in short supply. That was when it was backed by gold. That system ended way back in the last century. Since then, remember, all money is just a promise to pay. But also remember, the government has by far the best promise.

So, people who are cautious, like big pension funds, large companies, the wealthy and banks themselves want somewhere as safe to save as ordinary people – those with less than £85,000 in their bank account – have right now. And that means they want to save with the government.

But they can’t not in ordinary bank accounts. Because the government has set a limit in them. So the government has adapted, fairly surreptitiously, a gold standard era savings mechanism to meet this need for a safe savings account in the modern world of money.

That mechanism is ‘the gilt’. Gilt, of course, is gold. Once, these gilts were gold backed savings products. Not any more they are not, of course. Remember, everything about money is just a promise to pay now. Gilts, or government bonds, are like everything else in this regard.

And money is not scarce for the government now, either. It could have all it needs on overdraft at the Bank of England if it wanted. And it need not pay interest on that. So why doesn’t it go for this cheapest of all funding options? Because people need safety, that’s why not.

So, just as the government guarantees most people’s money in the bank, it also offers gilts (or government bonds) for those with millions or billions to save because they too want guarantees on their money. And they will accept a low rate of interest to get it.

Government bonds are not, then, real borrowing by the government. They are instead a savings mechanism. Sure, they look like a loan. But then so too is a building society bond a loan to a building society. But it’s also a savings account in reality.

And that’s what government bonds are: they are just savings accounts. That’s all. And, as I noted when I explained how money is created, savers’ money is not involved in money creation by lending, at all.

In the same way, government borrowing is not in involved in the funding of its spending. Sure, the government borrows. But then all savings institutions do, all the time. But they don’t lend savers’ money out. And the government doesn’t fund spending with borrowing either.

And before questions are asked about quantitative easing (QE) and where this fits in, let me address that one. QE is a process that involves the government buying back gilts. So, it is a mechanism to control the amount of savings it makes available. That’s it. No more.

QE also controls the amount of money in the banking system. QE forces money out of government gilts because the government buys them back, making them more scarce. The flip side is that government pays for these bonds using free money that the Bank of England creates for it.

This money creation puts more money into commercial banks, backing up the government guarantee that they will be solvent. That money injection is pretty important in that case.

But just to add to the list of what QE does, it also shatters the myth that governments are under the thumb of bond markets, for good. Now if bond markets get uppity about anything the government simply has the power to buy its debt back and bond dealers are left high and dry.

And another QE fact; by controlling the money supply into commercial banks the government gains almost complete control of short term interest rates, and through QE it has a massive influence on long term rates too. QE delivers protection from economic shocks as a result.

I’m not saying QE is a universal good, by the way. It’s forced money into the stock market, and overinflated it. That has increased inequality. Neither is good news. But it does add a powerful weapon to the government armoury for controlling the economy.

So, the government can now create money at will, control how much of that is in commercial banks and in government backed savings accounts at any time, control inflation through the tax system and deliver full employment if it wants, all if we understand money. Pretty cool, then.

But to make sure this is clear, where does this new knowledge that comes from the very simple understanding of how money is created (not printed, or made – created is the right word) leave us?

First, it says the government underpins the value of all our money, because whilst all money is a promise to pay, the government’s promise is the best, and our banks could not function without the support of that promise. We need to remind arrogant bankers of that, often.